Telling

It Like It Is Telling

It Like It Is

As Summer '09 Begins

We all know now that the global aviation

industry is clearly in a state of deep crisis.

It suffers from falling passenger and cargo

demand, excess capacity, rising fuel bill, and a host of other problems.

Rising fuel prices in the first half of 2008 plus a global recession in

the second half of 2008 wrecked havoc.

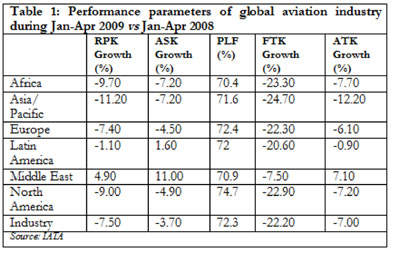

Data released by International Air Transport

Association (IATA) shows that revenue passenger kilometer (RPK) declined

by 7.5%; available seat kilometer declined by 3.7%; and passenger load

factor (PLF) was 72.3% during the period Jan-Apr, 2009—as compared

to same period of previous year. Similarly, freight tonne kilometer (FTK)

fell by a huge 22.2%; the available tonne kilometer fell by 7% during

the same period.

Regional performance data indicates that

Asia/ pacific suffered a decline of 11.2% in terms of RPK, and 7.2% decline

in ASK in both Africa and Asia/pacific region during the same period.

Africa plant load factor was very low at 70.4%, closely followed by the

Middle East (70.9%).

Interestingly, the Middle East was the

only region that recorded any positive growth in terms of passenger traffic.

However, freight traffic performance data indicated that all the regions

recorded declines. The Asia/Pacific region again led with a 24.70% decline

in terms of FTK and a 12.2% decline of ATK during the same period.

Interestingly, the Middle East was the

only region that recorded any positive growth in terms of passenger traffic.

However, freight traffic performance data indicated that all the regions

recorded declines. The Asia/Pacific region again led with a 24.70% decline

in terms of FTK and a 12.2% decline of ATK during the same period.

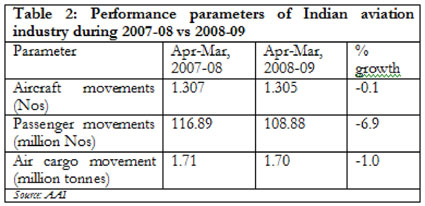

In India, the effect has been quite severe

on passenger traffic; in the global aviation industry the impact has been

most prominently felt in air cargo traffic. Passenger traffic has declined

from 116.89 million in 2007-08 to 108.88 in 2008-09, which translates

into a decline of 6.9%, according to Airport Authority of India (AAI).

Cargo traffic declined by 1%: from 1.71 million tonnes in 2007-08, to

1.70 million tonnes in 2008-09.

India‘s airport passenger traffic

data indicates that major airports saw declines in passenger traffic and

cargo traffic during 2008-09 as compared to 2007-08. Airports recording

a negative trend in passenger traffic include: Chennai (7.7%), Kolkata

(6.3%), Ahmedabad (10.6%), Trivandrum (7%), Mumbai (9.4%), Delhi (4.7%),

etc. Other airports —like Jodhpur (49.9%), Port Blair (38.2%), Jammu

(26.5%), Rajkot (16.7%), Amritsar (15.55), and Goa (13.9%) —have

also registered declines during this period. Among the factors contributing

to declining air travel was the number one cause: recession dampening

air travel demand, which depressed the numbers of international and domestic

tourists. A decline in air passenger traffic was seen in tourist centers

like Port Blair, Goa, Jodhpur and Amritsar etc. The decline in international

passenger traffic in Goa was 10.3%, Amritsar 2036%, and Gaya 10.7%. Domestic

passenger traffic declined for almost all airports.

India’s major airports such as Mumbai

(0.7%), Delhi (1.5%), Kolkata (3.1%), Trivandrum (1.6%), Ahmedabad (2.3%)

and Bangalore (11.3%) registered a decline in cargo traffic during 2008-09,

compared with 2007-08. This can perhaps be attributed to the generalized

slow down in international trade.

India’s major airports such as Mumbai

(0.7%), Delhi (1.5%), Kolkata (3.1%), Trivandrum (1.6%), Ahmedabad (2.3%)

and Bangalore (11.3%) registered a decline in cargo traffic during 2008-09,

compared with 2007-08. This can perhaps be attributed to the generalized

slow down in international trade.

IATA forecasts that the cumulative loss

of airlines will be US$9 billion in 2009. Total industry revenue of US$448

billion is projected for 2009—as compared with US$528 billion recorded

in 2008, which means a decline of 15%. Another risk underlined by IATA

is rising fuel prices, which could undermine any possible recovery in

the industry.

According to IATA estimates, the industry

needs US$6 trillion to recapitalize. IATA has however, cautioned that

banks are not able to finance the industry. IATA also points out that

changing business habits, reductions in corporate travel budgets, increased

use of video conferencing —all are dampening industry recovery.

India’s aviation industry is likely

to face a 6.8% fall in demand and 4% fall in capacity in 2009. This will

mainly be due to the rapid deterioration of global economic conditions.

India's international air services, which have increased three-fold between

2000-08, are now expected to witness 2-3% fall in demand, while capacity

may increase 0.7% in 2009.

A wide variety of steps have been undertaken

by airlines to address their problems:

•

Cutting capacity, laying off staff, deferring plane deliveries,

offering special schemes to lure the customers: these are commonly practiced

by airlines. For instance, Jet Airways cut capacity by 12% in 2008. The

CEO of Southwest Airlines, Gary Kelly, voluntarily cut his 2009 base salary

by 10%. Kingfisher Airlines has also cut 20% in the salaries of its pilots.

•

Airlines are working to use new technologies that change the

way planes fly. For instance, the global positioning information enables

shorter, more direct routes to destination. Special landing procedures—such

as continuous descent approaches —reduce fuel to the engines. Recently,

Southwest Airlines conducted a test flight using these technologies. They

found that it could reduce fuel consumption by 6%.

•

Aircraft manufacturers are trying to develop new engines and

lighter weight jetliners, both of which will help save fuel. The plane‘s

design and weight significantly affects the fuel consumption. This is

why the new jetliners—like the C-Series, the Boeing 787 and the

Airbus A350 – are all being manufactured using lighter-than-metal

composite materials.

Although the negative impacts of the current

global recession seem to be unavoidable, the aviation industry is trying

to reduce the severity of the impact. The industry is in survival mode

now, trying to do its best to manage through the current crisis. However,

global economic revival is what will finally hold the key for industry

recovery.

Gordon Feller |

Belgian

air freight carrier Cargo B has ceased all operations this Wednesday due

to lack of capital.

Belgian

air freight carrier Cargo B has ceased all operations this Wednesday due

to lack of capital.

Royal

Jordanian’s long-time CEO Samer Majali moving from Jordan to Bahrain

to become new Chief Executive Officer of local carrier Gulf Air.

Royal

Jordanian’s long-time CEO Samer Majali moving from Jordan to Bahrain

to become new Chief Executive Officer of local carrier Gulf Air.

Summer

Break

Summer

Break Aside

from any politics, the fact that President Barack Obama leads the

greatest country in the world we think makes all of mankind stand

a bit taller.

Aside

from any politics, the fact that President Barack Obama leads the

greatest country in the world we think makes all of mankind stand

a bit taller.